Trez Capital’s rigorous stress-testing framework and proactive risk management is driving attractive returns and stability in the private credit market

This article was produced in partnership with Trez Capital

Not all private credit is cut from the same cloth. With winners and losers bound to emerge, this is where the savvy managers step up. The ones armed with sharp due diligence and the muscle to stack their funds with prime assets and balanced leverage in rock-solid sectors have the edge.

As borrowers feel the heat, this prolonged higher-rate environment creates meaningful dispersion amongst managers. Not all private credit or alternative lenders play by the same rules, and the cracks are starting to show. The best private credit managers build resilient portfolios that cushion against the risks of high interest rates and a potentially slowing economy.

Trez Capital, a leading alternative investment manager focused on commercial real estate lending, exemplifies this shift with its robust approach to risk management and strategic adaptability. For over 25 years, Trez Capital has leveraged its expertise in private credit to deliver compelling returns to its investors while minimizing risk. Directing the risk framework are Christian Skogen, Chief Risk Officer; Keiju Yamasaki, Global Head of Credit Risk & Underwriting; and Clive Millar, Global Head of Asset Management.

Skogen emphasizes the importance of risk management in private credit markets, explaining, “Our active risk management framework is designed to protect our investors’ capital while seeking opportunities in a dynamic market.”

In response to evolving conditions, as Yamasaki highlights, Trez Capital has focused on high-quality and repeat-borrowers with proven experience, providing greater confidence against potential market and performance risks.

With increased pressure on borrowers due to cost inflation, robust risk management is crucial. To help mitigate risk, Millar points to Trez Capital’s active loan monitoring. In fact, Millar has personally relocated to Dallas, Texas, to be in-market to cover many of the firm’s development projects from the ground. Skogen highlights, “Good risk management is about the little things. Having Millar on the ground in markets we serve makes the difference when it comes to protecting our investors’ capital.”

Adjusting strategies in a high-interest rate environment

The higher interest rate environment brings both challenges and opportunities. According to Yamasaki, Trez Capital has “set new yield targets and adjusted our risk appetite to remain competitive.” With a focus on shorter duration loans—typically no more than three years and with an average tenure of 24 months—the firm is often financing construction and repositioning business plans. “Most of our loans are variable-rate, so as interest rates rise, the yields on our loans also increase,” explains Skogen. “We are capturing and participating in the upside as the benchmark rates go up, allowing us to offer higher yields to our investors.”

With a traditional bank, loans would either have a floating rate or a fixed rate. However, Trez Capital issues loans that have a floating rate with a floor—meaning while the loan rate will float upward as interest rates rise, they will not drop below a prescribed level as interest rates fall. Investors can benefit from upward rate participation, with downside protection within a defined range.

The firm’s loan book is further protected by maintaining a defensive Loan-to-Value (“LTV”) ratio, typically in the mid-60% to low-70% range, providing Trez Capital with a cushion against potential market corrections impacting the exit values of its loans. In the midst of a higher interest rate environment, the firm has benefited from rising rental rates in multifamily assets, which has offset some of the impact from increased financing costs, resulting in resilience in the portfolio.

The higher interest rate environment has placed challenges on developers, making many projects less profitable. Construction costs, labour costs, and insurance have all increased over the past 24 months, making it harder for developers to profitably move forward. However, there has still been ample opportunity to deploy capital with strong risk reward dynamics. Trez Capital typically originates loans in the $20 million to $80 million range. “In the lower end of that range, we used to compete with regional US banks,” Skogen notes, “But with the recent market shifts, regional banks in the US have retrenched, consolidating and stabilizing their balance sheets. This has reduced competition and led to fewer projects being financed. As a result, Trez Capital has been able to become more selective in choosing which sponsors and projects to finance.”

As interest rates start to come down, the volume of deals is now increasing. While there was a lower volume of deals available in the market earlier this year, Trez Capital is now seeing more opportunities emerge as rates come off. However, Skogen emphasizes that one of the key factors driving the market is the chronic housing shortage in both the US and Canada: “There is significant pent-up and structural demand for housing, and as rates stabilize, we expect more projects to turn profitable and come to market in the next 12-24 months. Developers are poised to meet this demand, and we are agile enough to respond quickly to the market shifts.”

Turning adversity into opportunity

As interest rates initially rose, Trez Capital responded by adjusting its guidelines allowing the firm to focus on high-quality sponsors and projects. “We saw developers who had strong liquidity and solid projects continue to move forward, even as regional US banks tightened their purse strings,” says Millar. “The US regional banks were asking for higher deposits to offset liquidity concerns that did not become part of the project and had to be held for the term of the financing pushing developers to look elsewhere for financing—often turning to Trez Capital. This shift meant that we were seeing stronger projects and better sponsors, even in a tough market.”

Millar highlights how this influx of quality borrowers strengthened the portfolio. While some areas of the market experienced stress, Trez Capital benefited from strong projects coming through the door. “This is how we build long-term relationships with repeat borrowers,” Millar asserts. “About 50% of our borrowers are repeat clients, and in Dallas, that number is closer to 80%. This consistency and trust come from being able to support strong borrowers, even during challenging times.”

The firm has developed numerous tools and institutional-grade processes to monitor loans, minimizing the need for asset managers to constantly shift focus. The objective is to automate as much as possible. This is why they employ in-house asset management professionals to thoroughly review and assess the loan portfolio on a monthly basis. If there are signs of elevated risk or cost overruns within the budget, these issues are addressed early and frequently. This proactive approach ensures nobody is left scrambling at the end of a project. Team members consistently evaluate the risk level throughout the project’s lifecycle.

Yield compression and managing investor expectations

With yield compression becoming a reality, managing reduced annual yields and investor expectations is a critical component of Trez Capital’s strategy. “We are enhancing yields without compromising risk management by leveraging our expertise to identify high-quality lending opportunities,” Skogen explains.

In an environment of constrained higher-cost capital, Trez Capital can dictate yield targets. Yamasaki explains, “We have the ability to say, ‘this is the kind of rate we need to charge,’ and we structure our loan participation accordingly to achieve the returns our investors expect.”

The process is highly dynamic, involving ongoing communication between the risk and origination teams. “Our feedback loop ensures that the origination team knows what we need from a return standpoint, and we adjust based on our risk appetite,” Yamasaki adds. This flexibility has been essential over the past 18 months, during which Trez Capital has retrenched in certain areas and carefully selected deals that provide the best risk-adjusted returns.

Trez Capital has been consistent about deploying capital in regions they fully understand, and continue to balance exposure across Canada and the US.

Proactive liquidity management: rigorous stress testing

For the past five years, the firm has been refining its sophisticated stress-testing framework, allowing it to capture and analyze vast amounts of data from both new opportunities and existing loans. Skogen recalls the advice he received early in his career: “I vividly recall the advice for a young aspiring risk executive was to utilize stress testing. But having the appropriate data to conduct insightful stress tests is key.”

Having a rich data set enables Trez Capital to not only understand how the portfolio is currently performing, but also allows them to anticipate how it will perform in the future. The key to effective stress testing lies in having well-considered outlook scenarios. It's essential to examine various possibilities and forecast how the portfolio might perform under each one.

The firm’s approach includes segmenting loans by vintage or geography to understand how different types of loans might behave under stress. This granular analysis helps in fine-tuning strategies to manage risk and optimize returns.

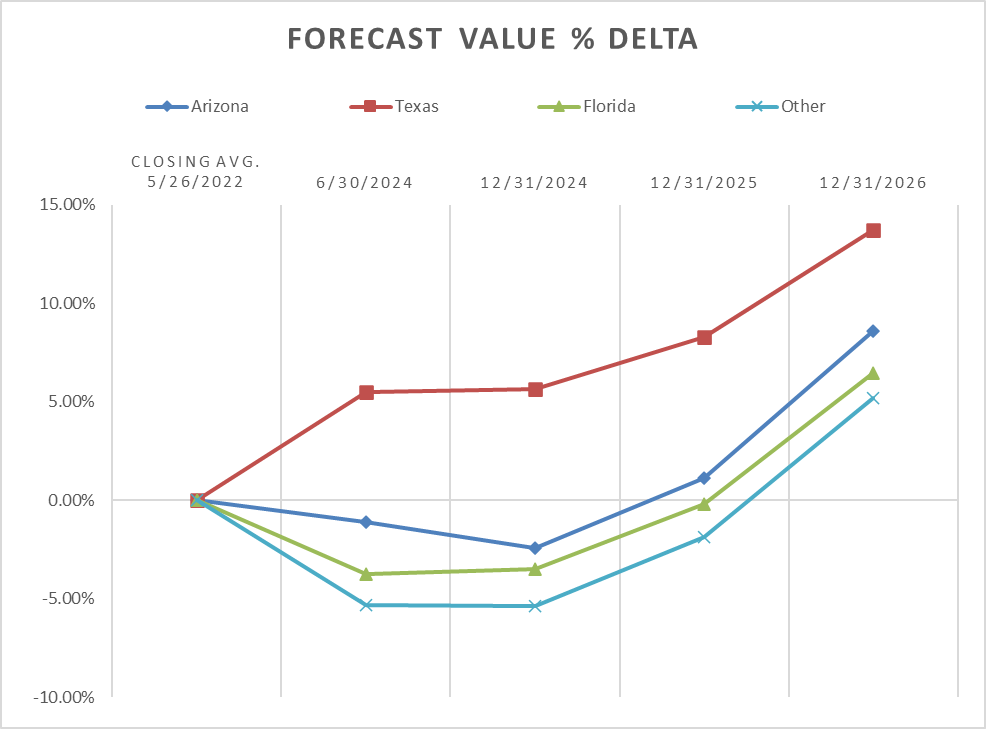

Although values have softened in the recent market cycle, Trez Capital’s core markets have been resilient and are forecast to strengthen as interest rates unwind. Chart from Trez Capital H1 2024 stress testing based on CoStar and JBREC data.

“From an underwriting perspective, sensitivity tools are the name of the game. We assess factors such as the income expected from the completed asset and the cap rates we’ll use once the project is done, typically within an 18 to 24-month window. Our goal is to be predictive, using current data to estimate what might happen by the time the project completes,” says Yamasaki.

Trez Capital relies on proprietary models developed in-house to forecast where rates will be and to ensure that project budgets are appropriate at the time of closing. In times of uncertainty, the firm can adjust the range of possibilities to assess how much the asset can withstand — either keeping the budget narrow in stable conditions or broadening when more uncertainty is anticipated.

On the flip side, if challenges arise, one of Trez Capital’s strengths has been underwriting the sponsorship—the owners and guarantors behind the loan. The firm evaluates liquidity to ensure the sponsors can step in and quickly address any issues that occur mid-loan. Trez Capital’s track record of working with top-tier and repeat sponsors gives investors confidence that they can rise to the occasion when needed.

Skogen emphasizes Trez Capital’s commitment to its investors: “If push comes to shove, we always protect our investors; we’re highly attuned to the fact that it’s not our money, it’s our investors’ capital, and we’ll always ensure they get the best possible outcome.”

Trez Capital works closely with its origination team to guide where to deploy capital, ensuring that every opportunity aligns with the firm’s broader risk appetite and balance exposure. Once opportunities are sourced, asset management becomes a critical aspect of execution. “At times, not everything will go according to plan,” Skogen notes, “but that’s where our in-house special loans team comes in, acting like the ER department of the firm, triaging and remedying loans that face challenges and navigating them back on track.”

Looking forward, Trez Capital is preparing for a dynamic real estate cycle, with both the US and Canada aspiring to solve chronic housing shortages in many sub-markets across both countries. The success of solving these challenges will be impacted by the near- and long-term economic growth, which will be influenced by the velocity and scale of interest rate moves by the Federal Reserve and Central Banks. Ultimately, Trez Capital sees increased opportunities for well-capitalized and strong developers across our core strategic markets in the US and Canada.

“Clients appreciate Trez Capital not just for the consistently attractive risk-adjusted returns, but because we are recognized experts in the field - we live, breathe and deeply understand real estate. We’ve built a solid reputation as trusted professionals for anyone involved in real estate development, offering deep industry knowledge and expertise that goes beyond the numbers,” said Skogen.