Canada life's reset option can help you capture market gains and reflect real-time value for your client

Canada’s demographic landscape is changing. Our population of seniors aged 85 and older is growing rapidly, set to nearly triple by 2050. As more Canadians prepare for retirements – and longer ones – financial stability during this life stage is coming into focus. For many, financial stability in retirement means not only being able to support their daily living but also to leave a meaningful legacy for their loved ones after passing on. For this, investments need to do more than hold steady, they need to grow.

Segregated funds may be a good investment option, as they come together with insurance protection to preserve savings. What you may not know is that you can add a feature to segregated funds offered by Canada Life that can further enhance their strength. This feature may be particularly relevant to your clients with retirement on their mind.

The guaranteed death benefit reset option

The backbone of segregated funds is the death benefit guarantee. It promises the investor’s beneficiaries a set payout regardless of market conditions. But Canada Life goes further, offering a guaranteed death benefit reset option. This unique feature automatically recalibrates the death benefit annually to reflect current market values and gives the investor the option to lock in market growth. The larger investment total becomes the amount protected by the investor’s chosen guarantees.

What’s more is that Canada Life recently enhanced the option by extending the maximum age to reset from age 70 to 80. This extended age limit is built for longer retirements. With this option added to a Canada Life segregated fund policy, you can help secure gains and help clients feel more confident about the legacy they’re building, for longer.

Bringing value to investors with a ‘set it and forget it’ safety net

There are many moving parts to keep track of when it comes to investments. Adding Canada Life’s guaranteed death benefit reset option to a segregated fund policy can mean one less thing to track. Think of it as a “growth capture” mechanism. It’s an effortless add-on that doesn’t require advisors or investors to monitor market cycles or decide on timing. It’s unlike similar products that require investors or advisors to keep tabs on market performance to manually trigger resets.

Simply put, with Canada Life’s unique reset option, each year, if the policy’s value is up, the reset locks in the gains as part of the new guaranteed amount. Not only can this feature help provide stability to an segregated fund policy, but it also helps navigate investors away from the uncertainty of market ups and downs, knowing each year’s growth is preserved in their legacy. It also helps make sure that beneficiaries receive the most up-to-date reflection of the investment’s success over time.

Maximizing a legacy through growth protection

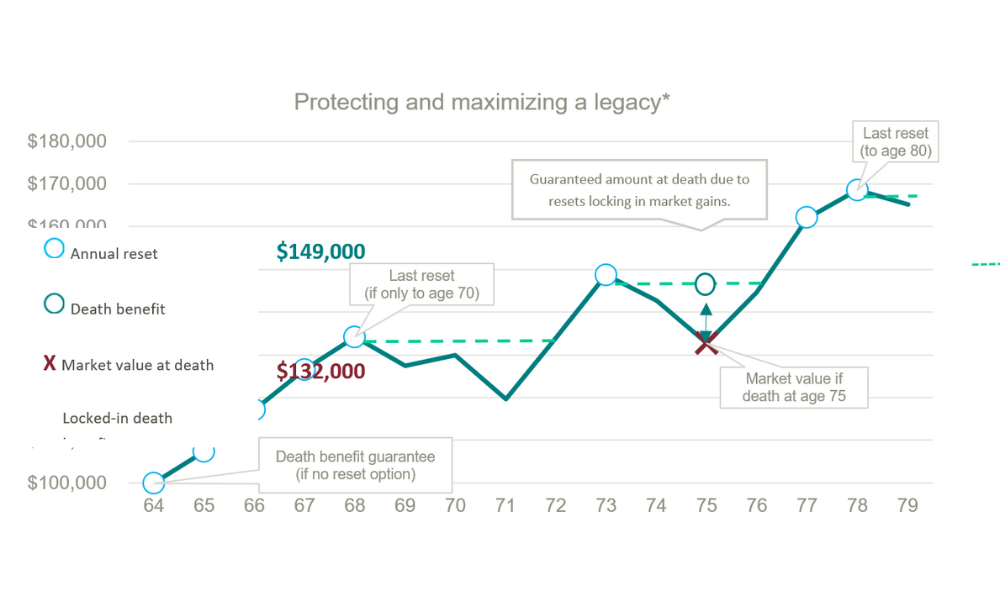

Consider Catherine, who at 64 is planning for her retirement. Catherine’s goal? To build an inheritance for her grandchildren and balance her need for growth with a sense of security. With this in mind, she opts to invest $100,000 into a Canada Life 75/100 segregated fund policy. She adds the annual death benefit reset option. By the time she’s 79, her policy has grown to $170,000 as a result of the reset option helping to capture and lock into market growth years.

If Catherine had passed away during a market downturn at age 75, her beneficiaries would have received her last locked-in reset amount of $149,000, despite the market value of the portfolio being only $132,000 at that time. This amount would make a significant difference to her grandchildren’s lives.

*Hypothetical market values for illustrative purposes only.

Start the conversation with your clients

Investors may be interested in the following unique advantages Canada Life’s reset option can add to their segregated fund policy:

Wealth protection: Investors can protect the value of their estate for their beneficiaries, as the option automatically locks in gains during market growth years, which are then protected from market downturns.

Higher growth potential: Investors may be able to tolerate more risk with higher growth investments and for longer, with confidence that gains will be preserved each year.

Flexibility: Investors can choose the reset option if it fits their needs. They can pay for this customized policy option for added protection if and when it aligns with their goals.

Help elevate your clients’ portfolios

With more Canadians preparing for retirement and markets becoming increasingly complex, the needs of investors are rapidly changing. It’s important that you and your clients are up to date on the tools available that can help meet their needs. The enhanced guaranteed death benefit reset option for segregated fund policies is one that you should know. Canada Life continues to show its commitment to providing innovative solutions that reflect the market landscape and changing needs of investors by offering it. This tool can help your clients who are thinking of their retirement years and the legacy they want to preserve, grow and pass down their wealth to their loved ones. Consider adding it to your toolkit when discussing with your clients how to help elevate their portfolio in a competitive market.

Disclaimers:

Canada Life and design are trademarks of The Canada Life Assurance Company.

You’ll find the detailed descriptions of the segregated fund policy in the information folder provided by your financial advisor. Any amount that is allocated to a segregated fund is invested at the risk of the policyowner and may increase or decrease in value.

In Saskatchewan, executors must disclose all known life insurance policies owned by the deceased including segregated fund policies. They must list the insurance company, policy number, designated beneficiaries and the value at the date of death.

The information provided is general in nature and should not be relied upon as a substitute for advice in any specific situation. For specific situations, advice should be obtained from the appropriate legal, accounting, tax or other professional advisors.