Locking in market growth with reset options can help clients grow and protect the value of their investments

This article was produced in partnership with Canada Life Investment Management

Canada's senior population is growing quickly, expected to triple by 2050. As Canadians plan for longer retirements, financial stability at this life stage, including supporting daily living and leaving a legacy for loved ones, may be top of mind. Therefore, investments need to grow, not just stay the same.

Segregated fund policies are a good investment option because they offer insurance protection and growth potential. Canada Life™ offers a feature that enhances these policies, especially for clients planning for retirement.

The death benefit guarantee reset option

The death benefit guarantee is the core of segregated fund policies. It ensures a set payout to beneficiaries, adjusted for any withdrawals. Canada Life offers a reset option for this guarantee, which updates the death benefit guarantee each year based on market values, locking in growth. This means the higher investment amount is protected.[1]

Canada Life has extended the maximum age to reset from 70 to 80,[2] catering to Canadians’ longer lives. With this option added to a Canada Life segregated fund policy, you can help secure gains for your clients and help them feel more confident about the legacy they’re building, for longer.

Effortless management with a 'set it and forget it' safety net

Investments can be complex. Adding Canada Life’s reset option to a segregated fund policy simplifies things. It acts as a “growth capture” mechanism, locking in gains each year without needing to monitor market cycles. This provides stability and preserves growth.

Maximizing a legacy through growth protection

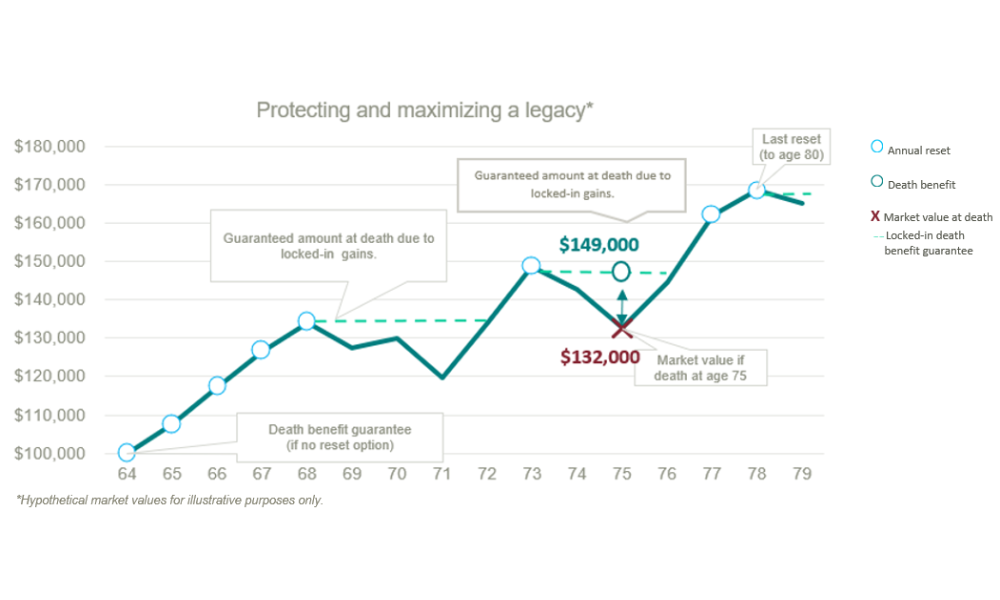

Consider Catherine, who at 64 is planning for her retirement. Her goal is to build an inheritance for her grandchildren while balancing her need for growth with a sense of security. She invests $100,000 into a Canada Life 75/100 segregated fund policy and adds the annual death benefit guarantee reset option. By the time she’s 79, her policy has grown to $170,000 due to the reset option capturing and locking in market growth years. If Catherine had passed away during a market downturn at age 75, her beneficiaries would have received her last locked-in reset amount of $149,000, despite the market value of the portfolio being only $132,000 at that time. This amount would make a significant difference to her grandchildren’s lives.

Start the conversation with your clients

Policy owners may be interested in the following advantages Canada Life’s death benefit guarantee reset option can add to their segregated fund policy:

- Wealth protection: The reset option automatically locks in gains during market growth years, protecting the value of the estate for beneficiaries.

- Higher growth potential: The reset option allows policy owners to tolerate more risk with higher growth investments, knowing gains will be preserved each year.

- Flexibility: Policy owners can choose the reset option if it fits their needs and pay for this customized policy option for added protection.

Help elevate your clients’ portfolios

As more Canadians prepare for retirement and face increasingly complex markets, the needs of investors are rapidly evolving. The death benefit guarantee reset option for segregated fund policies offered by Canada Life helps clients who are planning for their retirement years and wish to preserve, grow and pass down a meaningful legacy to their loved ones. By adding this option to your toolkit, you can help elevate your clients' portfolios in a competitive market.

Want to learn more about the death benefit guarantee reset option?

Contact your Canada Life Wealth Wholesaling team today.

Disclaimers

For advisor use only. Not for public distribution.

Canada Life and design are trademarks of The Canada Life Assurance Company.

A description of the key features of the segregated fund policy is contained in the information folder. Any amount allocated to a segregated fund is invested at the risk of the policyowner and may increase or decrease in value. These funds are available through segregated funds policies issued by Canada Life.

In Saskatchewan, executors must disclose all known life insurance policies owned by the deceased including segregated fund policies. They must list the insurance company, policy number, designated beneficiaries and the value at the date of death.

The information provided is general in nature and should not be relied upon as a substitute for advice in any specific situation. For specific situations, advice should be obtained from the appropriate legal, accounting, tax or other professional advisors.

[1] Guarantee amounts are reduced proportionately by any withdrawals.

[2] The death benefit guarantee reset option is subject to an extra fee at time of policy issue.