Learn how Canada Life RRSPs can benefit businesses and employees. Explore tax advantages, retention strategies, and setup tips

Established in 1847, Canada Life is considered as the country’s first local life insurance company. Since then, it has grown to become among the largest insurance and wealth management firms in the nation.

Among Canada Life’s offerings are registered retirement savings plans (RRSP). RRSPs are financial accounts that allow Canadians to save for retirement while reducing taxable income. This makes it an important tool for retirement planning.

In this article, Wealth Professional delves deeper into Canada Life RRSP. We will explore the different RRSP offerings, how they work, and what benefits they provide.

If you’re an employer working out whether Canada Life RRSP is the best choice for your employees, this guide can help. This piece can also be useful for employees who may be searching for other ways to save for retirement.

How does Canada Life RRSP work?

Registered retirement savings plans are designed to help Canadians achieve a financially secure retirement through a range of benefits. Canada Life RRSP is no different.

Just like in other RRSPs, the contributions made to a Canada Life RRSP are tax-deductible. Because of this, the investments grow on a tax-deferred basis until the funds are withdrawn in retirement when tax rates are likely lower. This immediate tax relief makes it easier for plan holders to build their retirement nest egg.

RRSPs are registered under the Canada Revenue Agency (CRA). The funds are allocated to different investment options. Also, individuals aren’t limited to a single savings account. If they choose to, they can open several RRSPs.

Get more information about how RRSPs work in this guide to registered retirement savings plans.

Types of Canada Life RRSPs

Canada Life offers various types of RRSPs:

Individual RRSP

Opened by the individual, this type of account is registered under their name. They also get full control of the investments.

If you plan to enrol in an individual RRSP, it’s best that you consult with a financial advisor first. This way, you can make an informed decision on whether it fits your financial goals.

Group RRSP

This serves as a savings and investment program set up by employers to help employees save for retirement. Employees can also get immediate tax benefits as the contributions are made before income taxes.

"Canada Life’s group registered retirement savings plans (RRSP) are made available through employers and plan sponsors," explained Kate Nazar, vice-president of group retirement services at Canada Life. "They can be an important part of a plan member’s overall compensation package and a valuable boost to the member’s future retirement income."

Group RRSPs work like individual RRSPs. The main difference is, Nazar added, group RRSPs can be tailored to fit the needs of each workplace. Through a group plan:

- employees can contribute directly through payroll deductions

- employers may choose to match a percentage of employee contributions

A Canada Life health and wealth consultant is available to help plan holders choose investments that fit their retirement goals and risk tolerance.

Joining a group retirement and savings plan is fast and easy. Canada Life offers online enrolment that provides tips and tools to help you along the way. Enrolment varies between plans. If your employer offers a group RRSP, you can talk to your plan administrator to find out how to join.

Spousal RRSP

This allows married couples, with one partner earning considerably more than the other, a way to balance their retirement savings. A spousal RRSP provides an income-splitting benefit for couples where the contributing spouse receives the tax deduction. This is while the account is registered under their partner’s name.

Learn more about how couples can make the most out of spousal RRSPs in this guide.

Canada Life RRSP contributions

In its RRSP insights and advice page, Canada Life recommends that plan holders come up with a contribution amount that matches their financial situation.

Plan holders have various options when it comes to making contributions. These include automatic payments through their bank accounts or regular lump-sum payments.

Another important factor to consider is the contribution room. This is the maximum allowable amount that plan holders can deposit into their RRSP in a given year. If an individual has more than one RRSP, the contribution room is combined with those of the other accounts.

CRA’s RRSP rules state that account holders can contribute whichever is lower of:

- 18 percent of earned income from the previous year

- $32,490 – the maximum contribution set in 2025

To qualify for an RRSP deduction, plan holders must make contributions during the tax year, or up to 60 days into the following year. Any unused contribution room from previous years can be carried over to future years.

Plan holders can contribute until December 31 of the year they turn 71 years old.

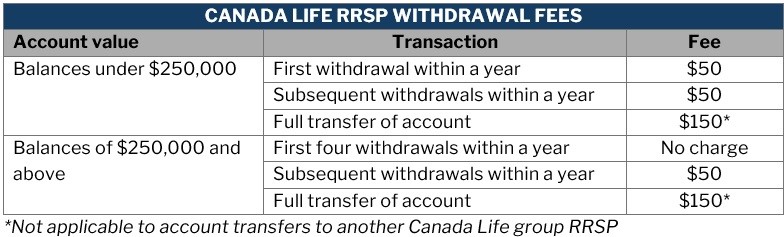

Canada Life RRSP withdrawals

Withdrawals from Canada Life registered retirement savings plans are taxed as income and may trigger withholding tax. But there are exceptions:

-

the Lifelong Learning Plan (LLP) allows account holders to borrow up to $10,000 a year to a maximum of $20,000 over four years to return to school full-time

-

the Home Buyers’ Plan (HBP) lets plan holders withdraw up to $60,000 to buy or construct their first home

This guide teaches you everything you need to know about using RRSPs to buy a first home.

Canada Life RRSP withdrawals are subject to fees, depending on the terms of the plan. These fees may be deducted from the withdrawn amount, depending on the account value and the frequency of withdrawal per year.

Here’s a summary:

Plan transfers

Canada Life also offers group RRSPs through its Freedom Financial NextStep program. This enables members to continue contributing to their group plan after leaving their jobs or retiring. It allows for a smooth transition into retirement with various retirement income options.

What sets Canada Life RRSPs apart from competitors?

Canada Life RRSP members can access a range of features and benefits to help maximize their savings. These include:

Online tools and resources

Plan holders can access a range of tools and educational resources to achieve their retirement goals, including:

-

Set My Goal: allows account holders to set and track their retirement income goals; they can also update their goals if their circumstances change

-

Contributions Calculator: shows users how extra contributions can boost their retirement savings

-

Income Wizard: provides helpful charts, graphs, and reports that show a person’s estimated income in retirement

This free online RRSP calculator can also prove useful for employers and employees who want to maximize their contributions.

Free well-being consultations

“Canada Life offers group plan members access to Canada Life health and wealth consultants at no additional cost,” Nazar said. “These are licensed professionals who can help members get started towards their retirement and savings goals.”

Canada Life’s health and wealth consultants can:

- assess the member’s needs and tolerance for investment risk

- give personalized insights to help maximize benefits

- offer proactive solutions to help improve financial circumstances

- help plan members make informed decisions that support their financial well-being

Financial literacy programs

Freedom on-site visits

Canada Life offers group plan sponsors on-site, in-person education sessions. A program called Freedom on-site visits, meanwhile, help plan members meet their financial goals.

Student Debt Savings Program

This program is designed for younger plan members. It allows them to pay down their student loans while receiving an employer match for payments that go directly towards their group RRSP savings.

Freedom Financial Registered Education Savings Plan

“Canada Life’s group RRSP offering includes an easy-to-access Freedom Financial Registered Education Savings Plan (RESP) option that is unique in the industry,” Nazar said.

“Plan members with a group RRSP can also choose to open an RESP account online within 10 minutes and set up regular, automatic contributions that will be eligible for federal matching grants.”

Performers

Canada Life offers specialized support to small businesses through Performers. This program provides small businesses with an easy way to get a group retirement and savings plan by working within their budget.

"Performers is easy to get started and administer," Nazar said. "There's no setup fee or ongoing administration costs to the sponsor. The plan is fully digital with online enrolment, contributions, and digital member documents."

What investment options are available for Canada Life RRSP?

Canada Life offers several investment opportunities for RRSP holders:

Mutual funds

A mutual fund pools money from several investors to purchase a diversified portfolio, which can include stocks, bonds, and other securities. A professional fund manager chooses the type of investment based on a specific objective.

One advantage of investing in mutual funds is that the risk of loss is reduced by spreading investments across a wide range of assets. This option, however, is available only for individual RRSP plan holders.

The table below lists the different types of mutual fund investment options in Canada Life:

|

CANADA LIFE MUTUAL FUNDS |

|

|---|---|

|

Asset class |

Investment mix |

|

Managed solutions |

Equities and fixed income securities

*As these investments are often in underlying funds, they are also diversified by investment style, geography, and investments within fixed income and equity asset classes |

|

Fixed income funds |

Government or corporate bonds |

|

Canadian balanced funds |

Equities and fixed income securities |

|

Global balanced funds |

Equities and fixed income securities |

|

Canadian equity funds |

Publicly traded equity issues of Canadian companies with above average growth potential |

|

US equity funds |

US equity securities |

|

Global and regional equity funds |

Stocks from companies around the world or in specific regions |

|

Sector equity funds |

Stocks from companies in specific industries or sectors of the economy |

Segregated funds

These are a type of pooled investment, much like mutual funds. But while mutual funds are typically sold by banks and investment companies, segregated funds are offered by insurance companies. A fund manager is responsible for choosing the investments in a segregated fund.

These managers select where to invest in based on the fund’s goals – like long-term growth or capital protection. This means no two segregated funds are the same. They have different investment mixes and because of this, perform differently over time.

The amount of return you receive from investing in segregated funds will also be impacted by the management fees and other associated costs.

Segregated funds are available as investment options for both individual and group RRSPs:

Individual segregated funds

Individual segregated funds offer both the potential for capital appreciation and some insurance benefits. Most segregated funds give you the option of a 75 percent to 100 percent payout of the premiums you paid. This is an advantage over mutual funds where you could potentially lose all your investment.

With individual segregated funds, you can also name a beneficiary. This can offer some protection against creditors. Upon your death, this also makes transferring of proceeds to your beneficiary easier.

Group segregated funds

Group segregated funds are the most common investment offered for group retirement and savings plans. They don’t have capital guarantees or offer the estate transfer or creditor protection benefits that individual segregated funds do.

Target date funds

"Canada Life retirement funds are part of Canada Life’s asset allocation fund offering and can be used by all investors, particularly, target date fund investors as they get close to or enter retirement,'' Nazar explained. "[This is] to provide more customized options than the one fund that’s currently provided at retirement in all target date fund suites."

Annuities

Canada Life offers annuities as part of its range of product options.

"Annuities can offer a guaranteed income stream with customizable options to help you step into retirement," Nazar explained. "Like a pension plan, an annuity can be thought of as pooling money from thousands of Canadians.

"You can put a portion of your retirement savings, like RRSP, into an annuity. It can cover your basic needs so the rest of your money can be used to live the retirement you want – taking that dream vacation, for example."

What other retirement saving plans does Canada Life offer?

Apart from registered retirement savings plans, Canada Life provides a range of products and services to help Canadian save for retirement. These include:

Registered pension plan (RPP)

This is set up by an employer to provide employees with retirement income. The plan is registered with the CRA, so employees can access tax benefits. Contributions made to an RPP are tax-deductible. Investment income also isn’t taxed until it’s withdrawn.

Employers are required to contribute to an RPP. Contributions are optional for the workers. RPPs may be structured as either a defined contribution or defined benefit plan.

Deferred profit-sharing plan (DPSP)

This is set up by employers as a way to share profits with their employees. Contributions depend on how much profit the company earns. Workers aren’t allowed to contribute.

DPSPs are registered with the CRA. They often serve as an alternative to a group registered pension plan.

Tax-free savings account (TFSA)

This works as a flexible investment savings plan that lets investors earn investment income and withdraw it tax-free. The savings can be used to:

- supplement retirement income

- purchase health or long-term care plans

- pay for major life events such as buying a house or pursuing continuing education

Non-registered savings plan (NRSP)

This provides investment opportunities for funds unrestricted by government regulations and contribution limits. Investment income earned in an NRSP is subject to taxes, but isn’t locked in.

Pooled registered pension plan (PRPP)

This is designed to provide low-cost retirement savings opportunities for employees and self-employed individuals who don’t have access to employer-sponsored plans. This guide explains what employers and employees need to know about PRPPs.

Voluntary retirement savings plan (VRSP)

This works almost the same as a PRPP. The plan is legally required for Québec employees who don’t have access to workplace pension. Check out this guide to voluntary retirement savings plans to learn more.

For more tips and strategies on how to maximize a registered retirement savings plan, visit our Retirement Planning News Section. Be sure to bookmark this page to access breaking news and the latest industry updates.

Do you think Canada Life RRSP has the features and benefits to help you build your retirement nest egg? Let us know in the comments

Related Articles:

Manulife RRSP: a guide for employers and employees

Desjardins group RRSP: a guide for businesses