How advisors can help clients with liquidity stuck on the sidelines

This article was produced in partnership with Canada Life Investment Management

High returns on risk-free or low-risk assets, combined with market uncertainties, have made it quite easy for clients to prefer staying on the sidelines rather than quickly re-entering the markets. Regrettably, when investors choose a conservative strategy and the market subsequently makes a sharp recovery, deciding the “right” time to re-enter can be quite challenging.

Consequently, some advisors grapple with how to assist clients who find themselves stuck with a substantial cash reserve and are hesitant to reinvest in equities, especially now that prices have risen. In some instances, these investors are even reluctant to reinvest in any asset class at all.

Even during generally bullish markets spanning the last decade, simply missing out on a few of the best days can diminish your clients’ overall wealth. It's important not to develop an attachment to cash akin to a love affair, as many investors did during the tumultuous period of 2008 to 2009. Instead, it's crucial to transition to a healthier, potentially more profitable relationship with your clients’ investments.

While fear may tempt your clients to stay out of the market, it's essential to recognize that such fears often don't align with market realities. Despite major historical events, the markets have consistently endured.

This is where the disciplined strategy of dollar cost averaging comes into play, especially relevant for investors in Canada where currently an unprecedented amount of cash sits idle on the sidelines.

What is dollar cost averaging?

Dollar cost averaging is a systematic investment strategy that involves regularly investing a fixed amount of money into a particular investment, regardless of the share price. Over time, this strategy can reduce the average cost per share of the investment, providing a cushion against market volatility. By purchasing more shares when prices are low and fewer when prices are high, investors not only optimize their entry points but also mitigate the risks associated with market timing.

Opting for dollar-cost averaging means relinquishing any attempt to time the market or pinpoint its absolute bottom. Many seasoned investors view this as a significant advantage. After all, history shows that attempting to catch a falling market has rarely led to fortunes but has instead resulted in substantial losses for many.

The advantages of dollar cost averaging

Dollar cost averaging offers several advantages for investors. First, it promotes commitment to a long-term investment plan, discouraging impulsive decisions driven by market fluctuations or emotions. Second, it reduces the risk associated with attempting to time the market by consistently investing over time, thereby lessening the impact of volatility on the portfolio.

Additionally, by automating investments according to a predetermined schedule, dollar cost averaging ensures emotion-free investing, with decisions guided by long-term goals rather than short-term market movements.

Finally, this strategy encourages disciplined investing, fostering a regular habit of contributing towards building wealth over time.

The risks of remaining on the sidelines and not participating in the market

For Canadians, the record high cash reserves – totalling $5.88 trillion in money market funds as of March 2024, a notable 24% increase from the previous year's $4.73 trillion – signify a caution that may be detrimental. The allure of cash, particularly with interest rates at 5%, is understandable, but it also means missing out on potential market gains.

Source: Morningstar Direct

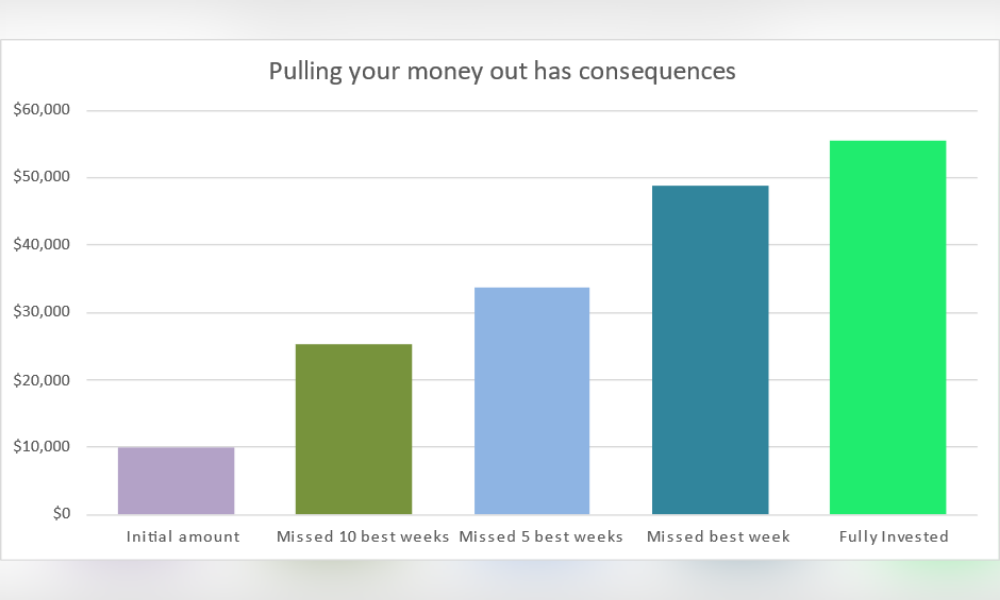

If your clients put $10,000 into the S&P/TSX 20 years ago and stayed fully invested they’d end up with $55,486 by Dec. 31, 2023. If your clients missed the best week, they’d end up with $48,753. If they miss the best ten weeks, they end up with $25,191 – less than half if they had stayed fully invested.

The segregated funds offered by Canada Life have consistently demonstrated robust performance and were notably recognized in 2023 with multiple FundGrade A+ awards. More than just investment vehicles, these segregated funds also offer insurance protection, which provides a safety net by guaranteeing1 a portion of the capital invested.

Unlike other investment options, a segregated fund policy is designed to provide certain guarantees, such as savings protection on the initial amount invested and estate benefits.

This dual benefit of investment and security aligns well with the principles of dollar cost averaging, providing an avenue for investors to re-enter the market with a methodical and secure approach.

In retrospect, one can identify opportune moments to buy assets at favorable prices. However, by the time such opportunities become apparent, it's typically too late to capitalize on them. Waiting on the sidelines to time asset purchases often leads to acquiring assets at prices that have already experienced significant appreciation, resulting in missed opportunities for substantial gains, and missing out on achieving long-term investment goals.

Choosing the right partner for your clients’ segregated fund investments is important. You and your clients deserve the best. We’re here to deliver just that. At Canada Life, we’re driven to provide best-in-class investment options from one of the strongest selections of segregated funds in the industry.2 Discover why we’re the right choice.

Have a question about the investment manager and their mandates? Contact your Canada Life Wealth Wholesaling team.

<disclaimer>

1 Guarantees apply at death and maturity. Guarantees are reduced proportionally by any withdrawals.

2 FundGrade A+® is used with permission from Fundata Canada Inc., all rights reserved. The annual FundGrade A+® Awards are presented by Fundata Canada Inc. to recognize the “best of the best” among Canadian investment funds. The FundGrade A+® calculation is supplemental to the monthly FundGrade ratings and is calculated at the end of each calendar year. The FundGrade rating system evaluates funds based on their risk-adjusted performance, measured by Sharpe Ratio, Sortino Ratio, and Information Ratio. The score for each ratio is calculated individually, covering all time periods from 2 to 10 years. The scores are then weighted equally in calculating a monthly FundGrade. The top 10% of funds earn an A Grade; the next 20% of funds earn a B Grade; the next 40% of funds earn a C Grade; the next 20% of funds receive a D Grade; and the lowest 10% of funds receive an E Grade. To be eligible, a fund must have received a FundGrade rating every month in the previous year. The FundGrade A+® uses a GPA-style calculation, where each monthly FundGrade from “A” to “E” receives a score from 4 to 0, respectively. A fund’s average score for the year determines its GPA. Any fund with a GPA of 3.5 or greater is awarded a FundGrade A+® Award. For more information, see www.FundGradeAwards.com. Although Fundata makes every effort to ensure the accuracy and reliability of the data contained herein, the accuracy is not guaranteed by Fundata.

For Advisors Use Only

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

A description of the key features of the segregated fund policy is contained in the information folder. Any amount allocated to a segregated fund is invested at the risk of the policyowner and may increase or decrease in value. These funds are available through segregated funds policies issued by Canada Life.