New analysis looks at multiple factors driving retirement security in 44 countries

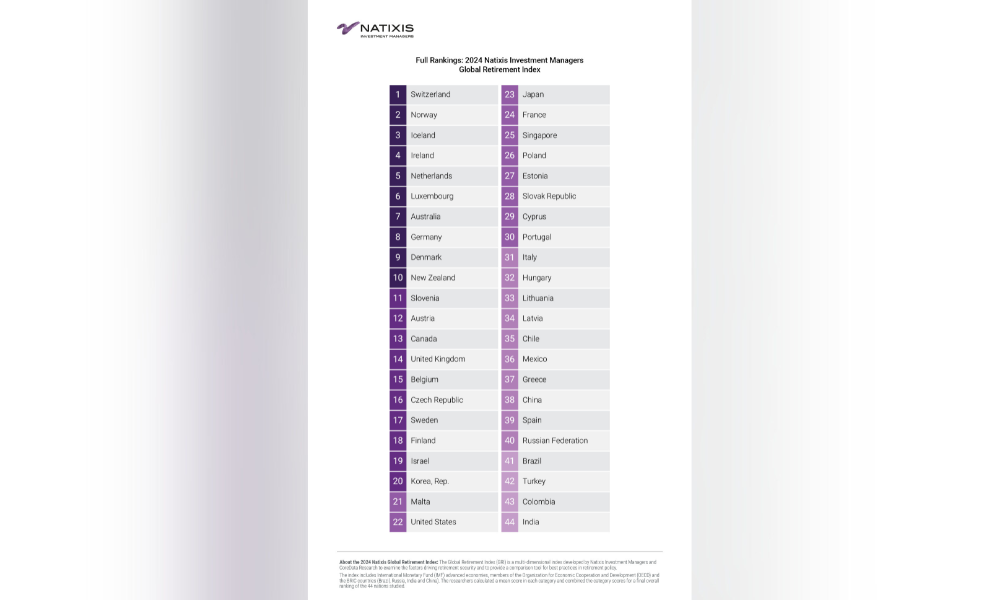

A global analysis of key factors that drive retirement security has seen Canada slip down the rankings in 2024.

The Global Retirement Index from Natixis Investment Managers shows that Canada is now 13th overall, down from 14th in 2023, as the material wellbeing element weighs on overall resilience of the country’s retirement landscape, mostly due to a rise in unemployment.

Globally, the study shows a stabilizing retirement outlook but it notes that individuals are feeling the pressure as more come to the realization that they are on their own when it comes to funding income later in life.

Apart from material wellbeing, Canada’s metrics are solid in areas such as the health sub-index which is boosted by life expectancy, quality of life, and finances – although its highlighted that the Bank of Canada has been less successful than some peers on making progress with inflation.

Canada also comes far higher in the overall rankings that the United States, which is 22nd having fallen two places, again mostly due to a decrease in the material wellbeing metric which has been impacted by rising unemployment.

However, the United States is leading all other countries in GDP growth at 2.5%, driven by an influx of immigration.

“Globally, we’ve seen a consistent set of results in this year’s index, though there is room for improvement to be made for most,” said Dave Goodsell, executive director of the Natixis Center for Investor Insight. “The United States continues to experience a ‘good news/bad news’ scenario for retirement security, with inflation slowly returning to normal while unemployment and public debt levels rise.”

The report was created in collaboration with Core Data Research.

Natixis IM’s Global Survey of Individual Investors found that 27% of respondents said that even if they saved $1 million, they still couldn’t afford to retire – that includes 24% of those who have already accumulated $1 million.

It also highlighted four key risks for individuals: interest rates, inflation, public debt, and investors themselves not making reasonable assumptions and realistic goals.

“As individuals increasingly take charge of their retirement planning amidst these challenges, financial service providers must become more proactive in supporting them,” Liana Magner, Executive Vice President and Head of Retirement and Institutional in the U.S. for Natixis Investment Managers. "To prevent future crises, it's crucial to offer personalized solutions that address both the current economic landscape and individuals’ specific retirement needs, including access to both public and private markets.”