Report says the significant borrowing is standing in the way of growth

The impact of Canadian government debt on the growth potential of regional economies has been highlighted in a new report.

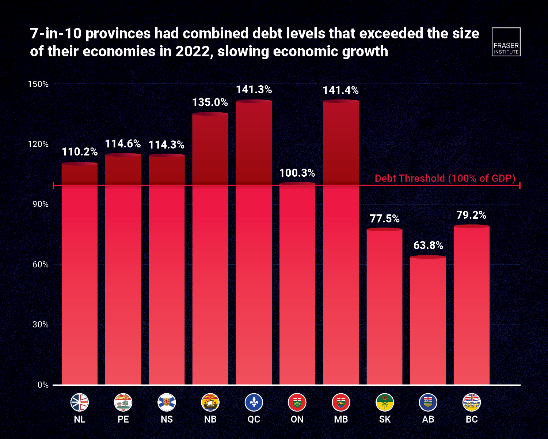

The Fraser Institute study found that seven out of the ten provinces had combined federal and provincial government debt burdens that were larger than their economies in 2022. The research also found that above 100% of GDP further borrowing does not support economic growth.

When government debt grows so high that it is larger than the entire value of the economy, not only does additional debt offer no benefit to economic growth, it actually hinders it and living standards stagnate,” said Jason Childs, a senior fellow at the Fraser Institute and author of The Effect of Government Debt on Economic Growth in the Canadian Provinces.

The report says that the negative impacts of high provincial debt burdens include weaker private investment and rising interest rates and inflation, all of which dampen growth potential.

Just three of Canada’s provinces had debt burdens less than 100% of GDP: British Columbia (79.2%), Saskatchewan (77.5%) and Alberta (63.8%) although concerns were noted in the report regarding the path of debt accumulation in BC.

At the other end of the scale, Manitoba had the highest combined debt-to-GDP level at 141.4% with Quebec close behind at 141.3% and New Brunswick at 135%. Newfoundland and Labrador, Prince Edward Island, and Nova Scotia were in the mid-range, while Ontario was hovering just above 100%.

“When our economies grow, Canadians benefit with higher living standards, but clearly large government debt burdens across the country are hampering those gains,” said Jake Fuss, director of fiscal studies at the Fraser Institute. “Policymakers should prioritize balancing their budgets and paying down debt to help spur greater economic growth for the benefit of all Canadians.”