Discover the pros and cons of being a DIY investor in Canada. Learn how to get started, choose the right tools, and build a successful self-directed investment portfolio

Many investors like being in charge of where they put their hard-earned money. And with easier access to online investment platforms, it’s not surprising to see a rise in the number of do-it-yourself (DIY) investors in Canada.

But investing is a serious business and if you’re new to the game, the learning curve can be steep. This begs the question, is DIY investing a smart move for beginners?

Wealth Professional gives you the answer in this client education guide. Here, we will discuss the pros and cons of being a DIY investor and dig deeper into why people choose to go this route.

If you’re at the start of your investment journey and working out whether a self-directed approach suits your financial goals, you’ve come to the right place. Keep reading and find out if the benefits of this investment style outweigh the risks in this guide.

What is a DIY investor?

As a DIY investor, the responsibility of building and managing your investment portfolio falls solely on your shoulders. This approach gives you more control over your investments. It also allows you to save on fees that you would’ve otherwise paid when getting the services of a financial advisor.

Because you direct your own investment strategy, you’re also referred to as a self-directed investor.

Just like other types of investors, DIY investors can access a range of investment products, including:

- stocks

- bonds

- mutual funds

- exchange-traded funds (ETFs)

- guaranteed investment certificates (GICs)

You can buy and sell these investment products through discount brokerages and online trading platforms. All you need to do is open a self-directed account, also called an order-execution-only (OEO) account.

Once done, you can tailor your investment strategy to suit your financial goals. You can typically choose between two approaches:

Active investing

This strategy involves a lot of buying and selling. As an active DIY investor, you try to maximize returns when the market is up and hedge your losses when the market is down.

Passive investing

This involves holding your investments long term. Instead of beating the market, you try to match its performance with different investment strategies.

As you have noticed, being a DIY investor involves a lot of market analysis and crunching the numbers. That’s why a certain level of understanding of how investing works is important for you to succeed.

If you’re new to the craft, this beginner’s guide on how to invest in Canada is a good place to start.

What are the pros and cons of being a DIY investor?

Many Canadian investors go the DIY route because of the sense of freedom this investment strategy provides. It also lets you cut costs as you no longer need to pay for the services of a financial advisor. But being a self-directed investor also means that you’re accepting the risks resulting from your own investment decisions.

Let’s go through some of the benefits and risks of being a DIY investor.

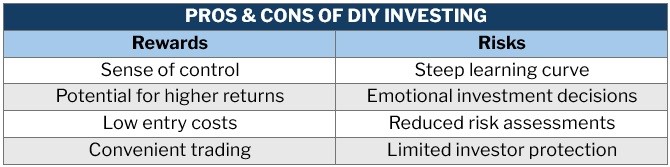

Pros of DIY investing

Self-directed investing offers several benefits, including:

1. Sense of control and independence

As a DIY investor, you can make investment decisions aligned with your values at your own time. You have total control of your trading, unless you choose to delegate some investment decisions to a professional.

Investing independently, however, requires a high level of understanding of how the market works. Even investors with years of experience set aside considerable time researching the market and managing their portfolio.

For new investors, it’s ideal to work with an experienced financial advisor like the five-star winners of our Best Financial Advisors and Professionals Under 40 awards.

2. Lower fees

DIY investing helps you cut costs. Apart from skipping advisory and management fees, you typically pay lower fees and commissions by making trades through a discount brokerage. These savings can potentially increase your returns.

The downside is that discount brokerages don’t offer personal financial advice and portfolio management services. If you’re an inexperienced investor, not having access to these types of services is risky.

3. Low entry costs

Some financial advisors only work with clients with a certain amount of assets. As a DIY investor, however, you can start small. There are many online trading platforms that don’t require a minimum deposit. This means you can start your investment journey regardless of how much funds you have on hand.

4. Convenience

Online trading platforms make it easier to buy and sell assets using your mobile devices. These platforms also provide access to trading tools and resources, including:

- educational materials

- stock prices

- trading information

- interactive performance charts

These allow you to track your investments in real time. If you want to learn more about how these tools work, you can check out this guide on how to start trading.

Cons of DIY investing

Being a DIY investor comes with its own share of risks. These include:

1. Steep learning curve

Investing has a lot of moving parts. If you want to make it on your own, you will need a deep understanding of how investing and the financial market work. You also need to do research on the different asset classes to find out which ones suit your investment goals.

If you’re starting from scratch, it may take you several months or even years to fully grasp these concepts. If you don’t have the benefit of time, then working with an experienced financial advisor may be your best option.

2. Impulsive and emotional decisions

Because of how easily you can trade on online platforms, it’s also easy to make impulsive decisions. If you want to succeed as a DIY investor, you need a certain level of restraint and discipline. You must be able to put your emotions aside and stick to your investment plan even when faced with poorly performing markets.

The Canadian Investment Regulatory Organization (CIRO) also warns against taking investment advice from social media.

“Do not trust anything you see on social media,” the group cautions on its website. “Lavish lifestyles can easily be faked, ‘proof’ of amazing investment returns can be doctored, and you never truly know who is on the other side of a direct message.”

3. Reduced risk assessments

Since you will be making investment decisions on your own, you don’t have the benefit of expert advice to tell you if the trade is in line with your investment strategy.

Most financial advisors have spent their whole careers understanding how to navigate markets and manage risks. If you don’t feel confident enough to do the same, then getting their services might be ideal.

If you’re based in Ontario, we compiled a list of the best financial advisors you can work with in this special report.

4. Limited protection

Many investor protections apply only if you’re working with a registered financial advisor. DIY investors aren’t always covered by these protections. That’s why it’s also important that you’re aware of your rights as an investor as laid down by the CIRO.

Here’s a summary of the pros and cons of self-directed investing:

Check out this list of investment types for first-time investors to find out which asset classes fit your risk tolerance and financial goals.

Why are more Canadians getting into DIY investing?

DIY investors make their own investment decisions without guidance from a financial advisor. While doing so requires time and effort, the learnings you make can help improve your overall financial literacy.

Recent studies reveal an increase in the number of DIY investors in the country.

-

A 2024 survey by the Canadian Securities Administration (CSA) has found that nearly half (45 percent) of investors have a self-directed account. About a third of these DIY investors opened their accounts in the past two years.

-

A 2024 report by the Conference Board of Canada reveals a decline in the number of investors working with financial advisors. From 2020 to 2024, the figures dropped from 69 percent to 61 percent.

-

A recent study by retail investor advocacy group FAIR Canada tracked a substantial rise in DIY accounts between 2020 and 2023. During the period, the number of self-directed accounts jumped from 2.3 million to 11.4 million.

Having more control over their investments and the substantial amount they save on fees are the top reasons why many Canadian investors are choosing the DIY approach, according to the reports.

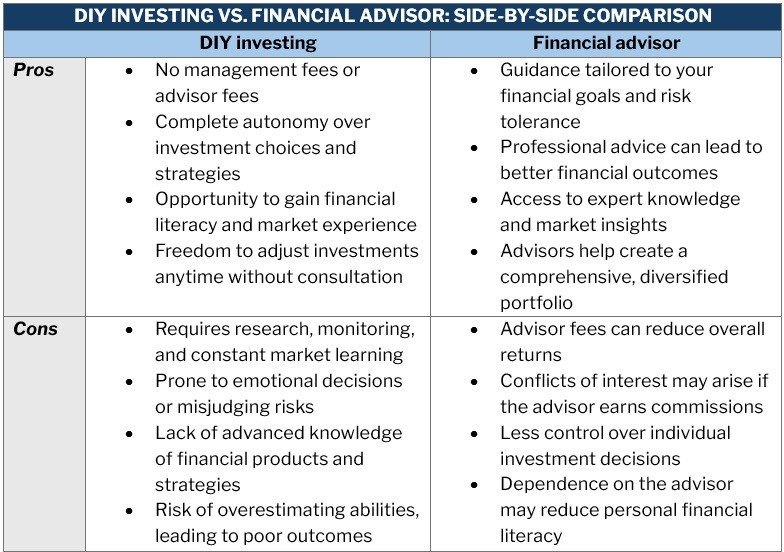

DIY investing vs. advisor: which one’s for you?

If you want to be in charge of your investment decisions and you find the sense of freedom that comes with a self-directed approach appealing, then DIY investing is for you. But there’s a catch – you must be willing to put in the time and effort to learn everything you need to know about investing and the financial markets.

Even so, there’s no guarantee that you won’t suffer a loss, especially in the event of market fluctuations.

If you’re just starting out, an experienced financial advisor can help guide you in making investment decisions that align with your risk tolerance and financial goals. You can also access certain protections not afforded to DIY investors.

Here’s a side-by-side comparison of the benefits and disadvantages of DIY investing vs. working with an advisor:

DIY and advised investing, however, aren’t mutually exclusive. You can choose to go with an investment approach that combines both. If you’re confident of your knowledge of mutual funds but less so of trading stocks, then you can DIY invest in mutual funds while letting an advisor choose stocks to buy or sell on your behalf.

Another option is using a robo-advisor. Robo-advisors use AI to choose investments that match your financial goals and situation. You may also allow robo-advisors to automatically pick investments without much oversight. This service comes with a fee that is often less than what a financial advisor would charge.

How to become a DIY investor

We can’t emphasize it enough – if you want to be a DIY investor, you need to educate yourself. Making investment decisions on your own requires you to have a clear understanding of what you are doing.

The CIRO explains it succinctly: “If you cannot explain the investment to a child, you probably don’t know enough about it.”

Online forums are replete with horror stories of DIY investing gone wrong, with some even losing several hundred thousand dollars of their hard-earned money.

Now, if you’ve put in the time and effort to understand how investing and the financial market work, you can become a DIY investor in Canada in a few simple steps:

-

Step 1: Find a firm to open your account with. Go with a firm that’s registered with the CIRO.

-

Step 2: Open a self-directed account. This is often free of charge, but you will be required to provide several personal and financial information.

-

Step 3: Fund your account. You can do so through several means, including bank transfers and cheques.

-

Step 4: Pick your investments. You have many options, including stocks, bonds, mutual funds, and ETFs. You can also invest in cryptocurrencies or choose to invest in real estate.

-

Step 5: Re-evaluate your investment strategy. Good investing entails adjusting your strategy based on the changes in your personal circumstances and market conditions.

Is DIY investing worth it?

DIY investing offers you more control over your investments, but it also leaves you entirely responsible for managing your portfolio. And while the potential returns may be higher because there are less fees and commissions to pay, it provides less protection in volatile markets.

As with any investment strategy, education is key to success. If you’re a new investor with little knowledge of how the market works, it’s best to enlist the services of an experienced financial advisor.

Our Best in Wealth Special Reports page is the place to go, if you’re searching for a reliable advisor to work with. The firms and professionals featured in our special reports have been handpicked by their peers and vetted by our panel of experts as trusted market leaders. By partnering with these industry leaders, you can be sure that your best interest comes first.

Do you think becoming a DIY investor is the right strategy for you? Tell us why in the comments