Once you decide to start investing, there are several factors you need to consider. This guide can help you jumpstart your investment journey

Investing can play an essential role in helping you build wealth and achieve financial independence. But if you’re just starting out, taking the first step on your investment journey can be overwhelming.

Newbie investors are often met with countless investment options and confusing jargon. These factors make the already difficult task of finding the right investment strategy even more challenging.

If you’re new to the industry and wondering how to start investing, this guide is for you. Here, Wealth Professional breaks down the basics of investing in Canada. We will walk you through the different types of investments and risks involved. We will also explain the various investment strategies, so you can pick the one that matches your investor profile.

To the financial advisers and portfolio managers who typically visit our website, this article is part of our client education series and can be a good resource to send to your clients.

How does investing in Canada work?

The Canadian Securities Administrators (CSA) defines investing as “putting your money to work, so it can make more money.” The investment process, however, isn’t as straightforward as the industry association’s definition.

Investors have no shortage of investment options. You can choose to invest in stocks, bonds, and mutual funds, just to name a few. While investing is among the most effective ways to see solid returns, there are no guarantees that your money will grow. When you invest, you also expose your money to risk as businesses shut down, market conditions fluctuate, and stock prices drop.

Investments in Canada are tightly regulated. Each province and territory has its own securities regulator. These supervisory bodies oversee investments and offer objective and interactive sources to help get you started with investing.

The table below lists the provincial and territorial securities regulators in the country. You can click on the links to access your jurisdiction’s regulating body, so you can start your investment journey.

How to start investing – provincial & territorial securities regulators in Canada

|

Province/Territory |

Regulating body |

|

Alberta Securities Commission (ASC) |

|

|

British Columbia Securities Commission (BCSC) |

|

|

Manitoba Securities Commission (MSC) |

|

|

Financial and Consumer Services Commission of New Brunswick (FCNB) |

|

|

Financial Services Regulation Division (under Digital Government and Service NL) |

|

|

Office of the Superintendent of Securities Northwest Territories |

|

|

Nova Scotia Securities Commission (NSSC) |

|

|

Office of the Superintendent of Securities Nunavut |

|

|

Financial and Consumer Services Division (under Department of Justice and Public Safety, PEI) |

|

|

Autorité des marchés financiers |

|

|

|

Financial and Consumer Affairs Authority of Saskatchewan (FCAA) |

|

Office of the Yukon Superintendent of Securities |

The regulators from Canada’s 10 provinces and three territories are all members of the CSA. As the industry’s umbrella organization, the CSA works to foster fair and efficient capital markets. It also protects investors across the country from unfair and fraudulent practices.

What factors should you consider before investing?

The CSA advises those starting their investment journey to have a solid understanding of how the process works.

“Whether you have an adviser or invest on your own, don’t invest in anything that you don’t fully understand,” the organization notes in this investment guidebook. “Take your time when making investment decisions and never sign documents you have not read carefully.”

These are the factors that you need to consider before taking the investment plunge:

Your financial situation

Assess your budget. This will give you insight into how much money you earn, where you spend it, and how much you save. Knowing where your money goes can help you make an informed decision on how much you have available to save or invest.

Your financial goals

Each investor has their own unique reason for investing. Some of the most common financial goals include:

- planning for retirement

- buying a home

- building an emergency fund

- saving for children’s education

- reducing debt

- achieving financial independence

Setting clear financial goals will give you an idea of how much money you will need to achieve them.

How long you want to invest for

Your choice of investment products must also align with what is referred to in the industry as “time horizon.” In layman’s terms, this is the period when you expect to hold your investment. As a rule of thumb, the longer the time horizon, the more money you should invest in risky investments. It’s crucial that you choose investments that are consistent with your time horizon. This ensures that you can weather downturns and benefit when markets recover.

Your risk tolerance

Risk tolerance is the amount of loss you are prepared to handle when making an investment decision. Ideally, you should only invest in products that you feel comfortable holding, considering the market fluctuations.

“In investing, the higher the potential return, the higher the risk,” the CSA said. “There’s no such thing as a high return, risk-free investment. If you want higher returns, you have to be prepared to accept the risks that go along with them.”

What are the different types of investments in Canada?

A big part of learning how to start investing is knowing the different investment products. This helps you diversify your portfolio, allowing you to take advantage of each product's strengths. A diverse portfolio also protects you from market fluctuations.

The CSA groups the different types of investment products into “asset classes.” An asset class is a group of investments that have the same level of risks. Here’s a list of these asset classes, along with the common investment options:

1. Cash and cash equivalents

This asset class includes money saved in your bank account and similar investments. The products in this group are considered safe investments and allow you to access cash whenever the need arises. The main drawback is that this type of investment has relatively lower rates of return compared to those in other asset classes. Some examples are:

- Treasury bill (T-bill): This is a type of guaranteed securities issued by the government to raise capital.

- Guaranteed investment certificate (GIC): This is a type of investment sold by banks and trust companies that provide a fixed rate of return.

- Money market fund: This is a type of mutual fund that invests in short-term fixed income securities.

2. Fixed income securities

One popular example of this type of investment is bonds. When you invest in fixed income securities such as bonds, you’re essentially lending your money to the government or a company for a set period. They are then expected to pay a fixed interest rate at certain times and repay the “face value” – normal dollar value in layman’s terms – at the end of the term.

You can often purchase fixed income securities through investment dealers. This type of investment is relatively safe as it comes with a guarantee. They tend to offer better rates of return compared to cash investments as you’re taking in more risks by lending your money for a longer timeframe.

3. Equities

Popularly known as stocks, these investment products entitle you to a share of ownership in a company. Stocks are bought for a share price. Depending on the company, this can range from a few to several thousand dollars. Stocks can also be purchased through mutual funds, which we will discuss next.

There are two ways you can make money from equities:

- if the stock’s value goes up

- if the company pays a dividend

However, there are no guarantees that either of these will happen. A stock’s value can rise or drop, depending on several factors, including:

- the company’s size

- the company’s profitability and financial stability

- the capability of the company’s management team

- general economic conditions

- market competition

- risk exposure

If you sell a stock for more than you purchased it, you will have a capital gain. If you sell for less, you will have a capital loss.

4. Investment funds

Investment funds work by pooling money from different investors. This allows you to invest in several products at a lower cost and leaves the investment decisions to a portfolio manager.

Investment funds can be set up as trusts, corporations, or partnerships. If set up as a trust or partnership, the funds are issued as units. If set as a corporation, investment funds are issued as shares. Just like in stocks, if you sell an investment fund, you can have a capital gain or a capital loss.

Here are some of the most common examples of investment funds:

- Mutual funds: These are professionally managed portfolios consisting of different asset classes such as bonds and stocks. Mutual funds are the most popular asset class in a registered retirement savings plan (RRSP).

- Exchange-traded funds: ETFs work like mutual funds, but with one main difference. These investment funds trade throughout the day like a stock and are purchased for a share price.

Learn more about how to invest in mutual funds in this guide.

5. Alternative investments

These investments may not be suitable if you’re just learning how to start investing because of their complexity. Alternative investments carry a higher risk, but they also bring a higher return potential.

Alternative investments are designed for seasoned investors and those with plenty of money to get specialized advice or take higher risks. Some examples of alternative investments are:

- futures and forward contracts

- income trusts, including real estate investment trusts (REIT)

- principal protected notes (PPN)

- hedge funds

- foreign currency, also known as Forex or FX trading

- cryptocurrency

Find out the basics of investing in cryptocurrency in this guide.

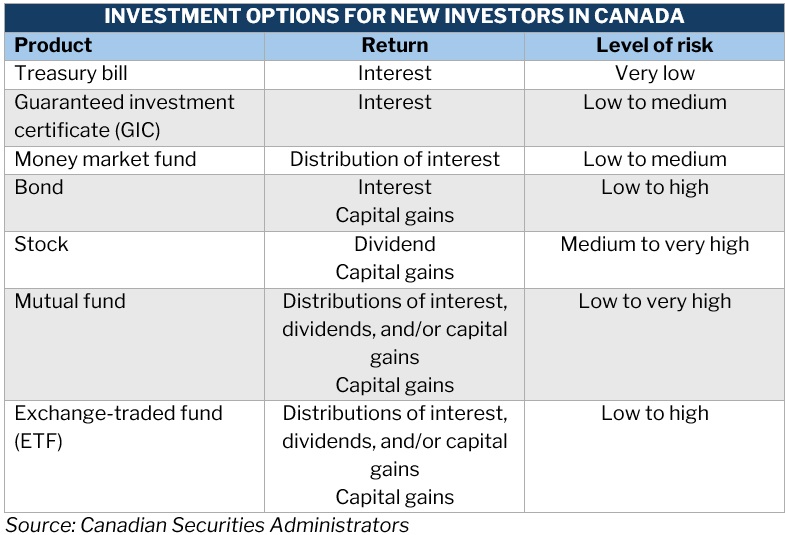

Here’s a summary of the different investment products, along with the type of return and levels of risk.

How much money do you need to start investing?

There’s no set amount required for a newbie investor to start investing in Canada. The amount of money you need depends on the types of investment services you use and the different investment products you choose to build your portfolio with.

If you choose to invest in mutual funds, for example, you will need an initial investment ranging from $500 to $1,000. For stocks, some brokerages require a minimum investment of $100.

What are the common ways to start investing?

Starting your investment journey entails picking the right strategy that will guide your investment decisions and help you identify which products to build your portfolio with. There are three common investment strategies novice investors can use:

1. Getting the help of a financial advisor

If you want a hands-off approach to your investments, enlisting the services of a financial advisor or portfolio manager is the way to go. These industry professionals will do the heavy lifting and make investment decisions on your behalf.

You can use this strategy if you don’t want to manage your investments but prefer a human touch in your investment decisions.

2. Accessing the services of a robo-advisor

A robo-advisor is an automated investor service made possible by artificial intelligence. This service uses sophisticated algorithms to determine your financial goals and risk profile, then bases its decisions on these factors.

This is the best route to take for new investors who prefer a hands-off approach but feel more comfortable entrusting their money to an AI-powered service.

3. Picking your own investments

You can choose to take full control of your investments through DIY or self-directed investing. This requires you to open an account with a brokerage firm and put together a portfolio of investments. You will need to have a certain level of investment knowledge as you will be solely responsible for monitoring your investments and making the necessary adjustments.

Another important thing to remember is that you’re not restricted to a single investment strategy. You can open investment accounts with different brokerages and use various strategies to manage your investments.

But if you choose to work with a financial advisor and you’re searching for one, our Best in Wealth Special Reports Page is the place to go. In our special reports, we feature only industry professionals who are nominated by their peers and vetted by our panel of experts as trusted and reliable market leaders.

Recently, we unveiled our five-star awardees for the Best Financial Advisors in Western Canada. By partnering with these specialists, you can be sure that your investments are well-managed, and your financial future is secure.

Did you find this guide on how to start investing in Canada helpful? Let us know in the comments.